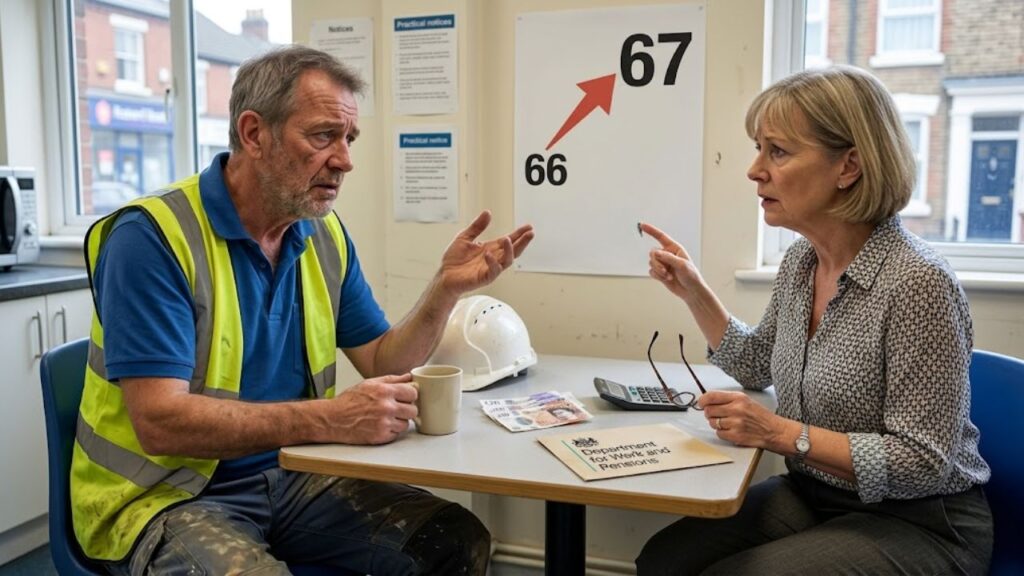

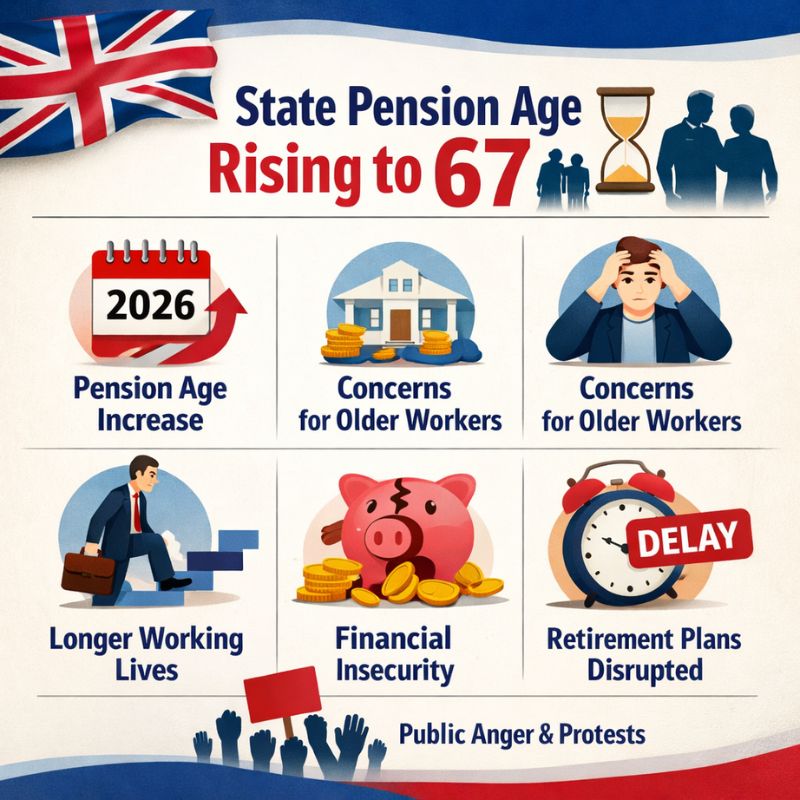

There is something significant about a change that arrives not with drama but with a birthday. Starting this week the state pension age begins rising from 66 to 67. This shift has been planned for years and widely discussed but it still unsettles those who see their retirement date moving further away just as they approach it. On the surface this seems like a sensible adjustment.

People live longer so the state pays pensions for longer. Something has to change. The numbers make sense because raising the pension age saves billions in a system facing demographic pressure. But numbers are not real life and the reality for people in their mid-sixties is much more complicated. This change reveals the gap between policy & people. For some the answer is straightforward.

Council Tax Surge 2026: Premium Charges Could Push Bills Up to £27,000 for Some Properties

Council Tax Surge 2026: Premium Charges Could Push Bills Up to £27,000 for Some Properties

They can work a bit longer and retire a bit later. Some will do exactly that by staying in their current jobs rather than starting new careers. But for many the extra year is not an opportunity but a problem. It creates a period where income drops and health may decline. The truth is that the ability to keep working is not evenly spread. It depends on your job and your health and frankly where you live.

Especially in poorer coastal and former industrial areas life expectancy and healthy life expectancy lag far behind wealthier areas. A man in Blackpool might expect little more than six years of state pension payments compared with a decade for women in Kensington and Chelsea. A uniform pension age applied to an unequal country produces unequal results. Meanwhile people in their twenties watch with concern. Officially the pension age is set to rise to 68 in the mid-2040s.

But few seriously believe it will stop there as reviews suggest further increases. The message is clear. Plan for 70 and hope for the best. Yet planning becomes harder in such an uncertain landscape while also paying off student loans. If the target keeps moving how do you plan the journey? Do you save more or work longer or simply assume the state will provide less? The risk is a gradual loss of trust in the system itself. One solution is abandoning the idea that a single pension age fits everyone.

If longevity and health vary so widely perhaps entitlement should too. A more flexible system that allows earlier access for those in poorer health or physically demanding jobs would better reflect the country as it actually is rather than as spreadsheets assume it to be. There is also a case for staggered financial support through targeted benefits or partial pensions that recognize the grey zone between full-time work and full retirement.

The current cliff edge of working one day and receiving a pension the next feels increasingly outdated compared to modern working lives. None of this is simple and none of it is cheap. But the current situation is not cost-free either in economic or social terms. The rise to 67 is not the end of the story but the beginning of a longer debate about what retirement means in 21st century Britain that is ageing and unequal and still adjusting to both. We are going to live longer and we are going to work longer. That much seems certain. What remains uncertain and urgently worth debating is how we do so fairly.

DWP Benefit Rule Changes 2026: New Requirements Impact PIP DLA Attendance And Carer Allowance

DWP Benefit Rule Changes 2026: New Requirements Impact PIP DLA Attendance And Carer Allowance