April marks a significant period of change for state pensions, as pensioners are set to see an increase in their weekly amounts. Those receiving the full new state pension will notice a rise from £230.25 to £241.30 per week. Similarly, individuals on the full basic state pension will see their weekly income increase from £176.45 to £184.90.

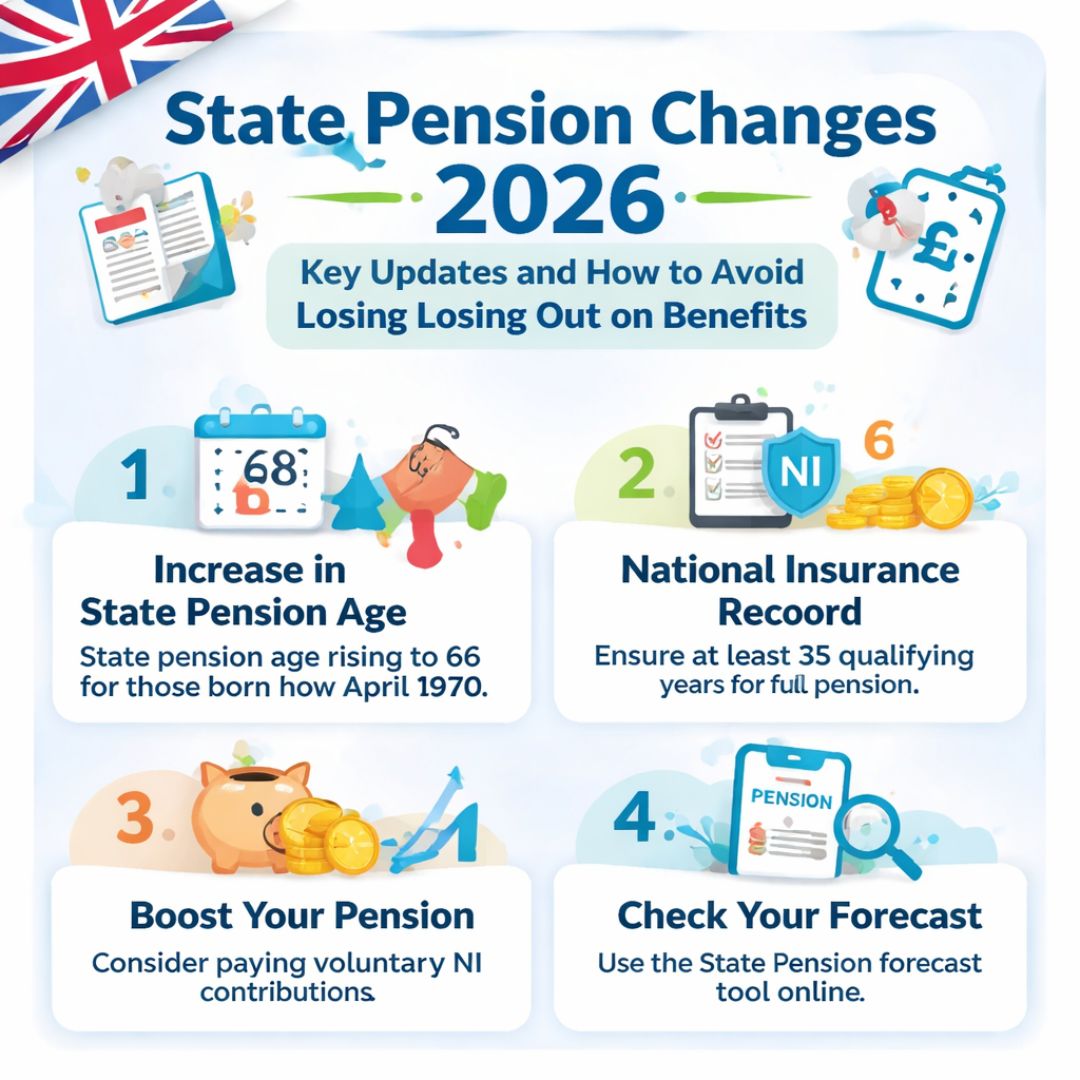

However, less commonly known is the gradual rise in the state pension age. Starting this April, the state pension age will increase and will reach 67 by April 2028. This change may come as a surprise to some, especially for those who had planned their retirement around the previous age.

The state pension serves as the core of many people’s retirement plans. If you’ve been planning to retire at 66, only to discover that the state pension age has shifted to 67, it could cause significant disruption to your retirement timeline. A quick check of your state pension age on the gov.uk website could prevent any unexpected issues.

DWP Benefit Rules 2026: Four New Changes Introduced for Universal Credit, PIP and ESA Claimants

DWP Benefit Rules 2026: Four New Changes Introduced for Universal Credit, PIP and ESA Claimants

State Pension Age Review and Future Changes

It’s important to note that this is not the final increase. According to the current schedule, the state pension age will start rising towards 68 in 2044. However, there is an ongoing review, and it’s possible that this timeline could be adjusted in the coming years. This means we may see the pension age increase even sooner, or a new timetable could be introduced for further changes.

Challenges of Increased State Pension Age

The rise in state pension age presents several challenges, particularly as we face longer life expectancies but not necessarily better health. As discussed in past columns, many individuals will not be able to continue working well into their mid-60s, let alone their late 60s or beyond. This leaves the question: how will individuals who can no longer work fill the gap between retiring and accessing their state pension?

Impact on Pension Planning

This shift underscores the importance of early pension planning. We are living longer but not necessarily healthier, so there’s a need for people’s pensions to last longer. However, many will have less time to contribute to them. It’s crucial to boost pension contributions while still employed to ensure financial security in retirement.

Potential Solutions for Longer Working Life

On a positive note, the auto-enrolment scheme is helping more people build their pensions by contributing throughout their careers. Nonetheless, more needs to be done. In the long run, supporting people in staying employed longer through retraining opportunities and more flexible roles could be a key factor in improving pension outcomes.